Ask any DMC founder what the gross margin was on their last 200-pax incentive trip and you'll get one of three answers: a confident percentage that turns out to be 6 points off when finance closes the books, a vague "around twenty-something", or "let me check and get back to you". The third answer is the most honest. It also signals the core problem with how event profitability is tracked in most MICE businesses — you find out after it's already too late to do anything about it.

By the time the post-event invoice is raised, the final supplier bills have landed, and finance has reconciled the GST input, the event has been over for three to six weeks. The salesperson has moved to the next pitch. Operations is already deep in a new run sheet. If the margin came in at 14% instead of the 24% you quoted, no one is going back to find out why. It gets absorbed, the lesson gets lost, and the same leak shows up on the next event.

The fix is not better reporting after the fact. The fix is visibility at three distinct phases: before the event, when margin is locked in by the quote; during the event, when cost creep happens in small decisions no one is tracking; and after the event, when collections, sign-off, and reconciliation determine whether the margin survives to the bank account.

Before the Event: Margin Is Decided in the Quote, Not at Close

The most common misconception in MICE finance is that margin is determined by execution. It isn't. By the time the client signs the proposal, the maximum possible margin on the event has already been set. Everything that happens after is either preserving that margin or eroding it.

This is why a sloppy quote is a more expensive mistake than a sloppy operation. Three things in the quote phase determine whether you've locked a real margin or a paper one:

Supplier rates have to be current, not remembered. A hotel quote from four months ago does not predict today's rate. A coach vendor who quoted ₹18,000 per day for a Bangalore-to-Coorg run in October is not going to honour it in January when fuel prices have shifted and his fleet is booked into wedding season. If your quote uses old or unverified rates, the gap shows up at the supplier-invoice stage — and by then it's a margin problem, not a quoting problem.

GST has to be calculated at the correct rate per category, not flat. Hotel rooms above ₹7,500 tariff attract 18%, below attract 12%. Domestic economy flights attract 5%. Bundled F&B in an event package attracts 18%, not the 5% restaurant rate. Apply 18% across the board and you've either inflated the quote (losing the deal) or you've absorbed the difference yourself (losing the margin). A 200-pax event with mixed components can easily have ₹80,000 to ₹1.5 lakh of GST miscalculation in either direction.

Multi-currency exposure has to be hedged or priced in. International incentive trips quoted in INR but paid out in AED, USD or THB carry currency risk between proposal and supplier payment. A 4% INR depreciation against the dollar between quote and payment is a 4% direct hit on the foreign-cost portion of the event. On a ₹40 lakh Dubai trip where ₹22 lakh goes to AED suppliers, that's ₹88,000 of margin gone without anyone making a mistake.

The operators who consistently close events at their quoted margin are the ones who treat the quote as a financial document, not a sales document. Their pricing comes from a live quotation system connected to current supplier rates, with category-correct GST applied automatically, not from a salesperson's best estimate at midnight before the deadline.

During the Event: Cost Creep Lives in the Small Decisions

The "live" phase is where most operators lose visibility entirely. The quote is signed, the advance has come in, the run sheet is in motion — and from that moment until the final invoice, margin is tracked in someone's head or in a WhatsApp thread.

This is where cost creep happens. Cost creep is rarely a single bad decision. It's twenty small ones, each defensible on its own, that compound into a margin hit no one sees coming.

Examples from the live phase of a typical 3-day corporate offsite:

- The client requests a late-night snack on day two. F&B says "we'll arrange it." That's ₹600–900 per pax uncovered. On 180 pax, ₹1.1–1.6 lakh.

- The leadership team decides to extend a session by 90 minutes. Coaches that were due to leave at 6pm leave at 8pm. Driver overtime, per coach per evening, runs ₹2,000–4,000. On four coaches, ₹16,000.

- A VIP guest is upgraded from Deluxe to Suite mid-stay. Differential rate of ₹12,000 per night × 2 nights, plus 18% GST. ₹28,000.

- The AV vendor adds two extra wireless mics for a panel discussion. ₹15,000.

- The team-building vendor charges a "weather contingency" fee that wasn't in the original quote because the activity moved indoors. ₹35,000.

None of these are scandals. Each one is a sensible call in the moment. But together, on this one event, they've eaten ₹2 lakh of margin — and the salesperson who quoted the event has no idea any of it happened.

The discipline that prevents this is not refusing client requests. It's recording every cost decision against the event in real time and flagging when actual costs cross a threshold of quoted costs. If the F&B line was quoted at ₹4.8 lakh and live costs cross ₹5.1 lakh, the operations lead and the account manager both need to know — before they approve the next add-on. A connected operations and run sheet system tied to the same line items as the quote is what makes this visibility possible. A spreadsheet updated weekly is not.

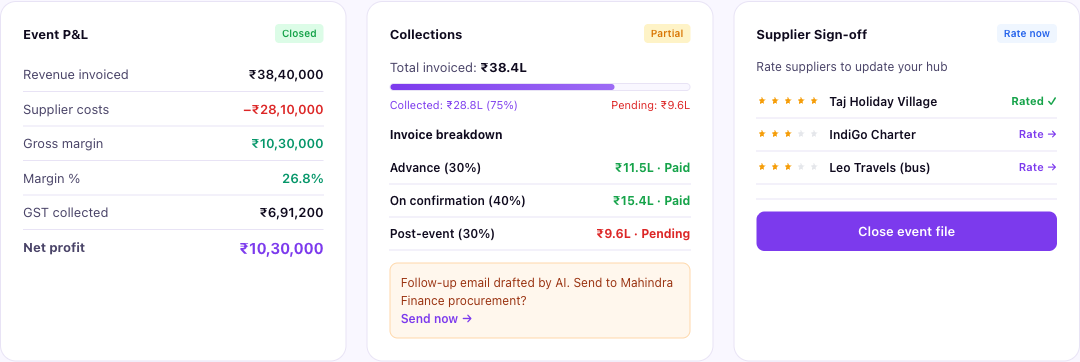

After the Event: Where Quoted Margin Becomes Banked Margin

Most operators consider the event closed when the last guest checks out. Financially, the event is nowhere near closed. The gap between event-end and the cash actually hitting your account is where the final margin is determined — and where a surprising amount of it gets lost.

Three things have to happen in the post-event phase, in this order:

Final supplier reconciliation. Compare what each supplier quoted, what they invoiced, and what was actually delivered. Hotels add resort fees, banquet service charges, or "additional services" that weren't in the contracted rate. Coach operators bill for waiting time, toll, parking. Foreign vendors invoice with FX rates that differ from your booking rate. Every variance between quoted supplier cost and invoiced supplier cost is margin movement — usually downward. Catching it requires line-by-line comparison, not a glance at the total.

Collections discipline. A typical Indian MICE invoice structure is 30% advance, 40% on confirmation, 30% post-event. The advance and confirmation tranches usually arrive on time because the client needs the event to happen. The post-event 30% is where defaults concentrate. The client has already had the event, the photos are on LinkedIn, and your leverage is gone. Add the standard 60–90 day payment terms most Indian corporates work to and you're looking at receivables aging that quietly eats your margin to working capital cost. GST on advance is owed on receipt under Section 13 of the CGST Act — meaning you've already paid output GST on money you may now have to chase for six months.

Supplier sign-off and feedback. This sounds operational, not financial — but it isn't. Sign-off is when the supplier confirms their final invoice matches the agreed scope. Skip it, and a supplier comes back six weeks later with a "missed item" you can no longer dispute because the event is closed. Rating suppliers post-event also builds the institutional knowledge that prevents margin leaks on the next event — a coach vendor who consistently overbills on waiting time should be flagged in your hub, not re-quoted for the next job.

When this phase is run cleanly, you get a closing P&L that looks like this:

Revenue invoiced, supplier costs, gross margin, GST collected, net profit — all reconciled against the original quote, with collections status and supplier sign-off visible in the same view. That's not a finance report. That's an operational dashboard that lets you close the event file with confidence and move on. It's also what makes the next quote you write better — because you now know what your real margin was, not what your quoted margin was.

What "Good" Margin Actually Looks Like for Indian MICE

Margin benchmarks vary by event type and destination, but reasonable ranges for the Indian market sit roughly here:

- Domestic corporate offsites and conferences: 18–25% gross margin. Above 25% usually means strong supplier negotiation or a long-standing venue relationship. Below 15% means either heavy price competition or undetected cost creep.

- Domestic incentive trips: 22–30% gross margin. Higher because experiential components and customisation command premium pricing, and clients are less price-sensitive than they are on conferences.

- International incentive trips (short-haul: Thailand, Sri Lanka, Dubai): 15–22% gross margin. Foreign supplier costs and FX exposure compress margin, but volume per event is higher.

- International incentive trips (long-haul: Europe, US, Australia): 12–18% gross margin. FX and air component dominate cost structure.

- Weddings and social MICE: 25–35% gross margin. Less procurement discipline from the client side, more room for premium positioning.

Net margin — gross margin minus your operational overhead (sales salaries, ops team, software, office, GST handling time) — typically runs at 8–15% of revenue for well-run MICE businesses in India. Operators consistently below 6% net are either pricing too aggressively, running expensive sales cycles, or absorbing cost creep they can't see.

The point of these benchmarks isn't to defend a number. It's to know which event types in your portfolio are pulling the average up and which ones are pulling it down — and to make portfolio decisions based on closing margin, not on revenue.

The Discipline Behind Operators Who Know Their P&L Early

The DMCs and PCOs who can tell you the net profit of an event the day it closes — not three weeks later — aren't doing anything magical. They've built three habits.

One: every line item exists in one system, from quote to invoice. The quoted F&B cost, the live F&B cost, and the invoiced F&B cost are the same record, updated through the lifecycle. No re-entry, no reconciliation between Excel and accounting software, no orphan line items added on WhatsApp.

Two: actual costs are recorded against the event as they happen, not at the end. When the suite upgrade is approved, when the late-night snack is added, when the coach overtime kicks in — each one is logged immediately. By event close, the P&L is 90% built.

Three: closing the event is a checklist, not an aspiration. Final supplier invoices in, supplier ratings updated, collections schedule confirmed, GST reconciled, file closed. Three days post-event, not three weeks. The next event isn't started until the previous one is closed.

This is what an AI-native operations system is built to enforce — not because operators are sloppy, but because the volume and variability of MICE events makes manual tracking break down at scale. The operators who run ten events a quarter on Excel can survive. The ones running thirty cannot.

If you can't tell me the gross margin on the last event you closed, the problem isn't that you don't know the number. The problem is the system you'd need to look it up in doesn't exist yet.

MiceStack is the AI-native operations platform for MICE businesses in India — pipeline, quotations, run sheets, and GST invoicing in one system. Start free →